The views expressed are those of the authors at the time of writing. This information does not constitute, and should not be construed as, an offer of advisory services, securities or other financial instruments, a solicitation of an offer to buy any security or other financial instrument, or a recommendation to buy, hold or sell a security or other financial instruments in any jurisdiction.

By The HighVista Private Credit Team

Executive Summary

AI is forcing investors to revisit a question many thought was settled: how durable is the software business model when the economics of development, distribution, and competition are being rewritten in real time? For private credit investors, the implications are asymmetric—uncertainty matters more when upside is capped and downside risk is permanent.

In this paper, we outline why markets are struggling to price software and software‑exposed credit—and how that uncertainty translates directly into underwriting and capital protection:

- We revisit the three assumptions that historically made software attractive to lenders—front‑loaded development costs, exceptional gross margins, and highly recurring subscription revenue.

- We examine how AI pressures all three pillars at once, resetting R&D investment cycles, embedding ongoing compute costs, and potentially eroding customer stickiness through new workflows and interaction models.

- We translate these shifts into credit terms, explaining why rising dispersion and multiple compression may impact lenders, particularly where leverage is elevated and repayment depends on refinancing or exit outcomes.

- We conclude with how this framework informs HighVista’s approach to private credit—emphasizing patience, disciplined underwriting, and the pricing required to engage in today’s software dislocation with appropriate downside protection.

Trouble in Software-Land

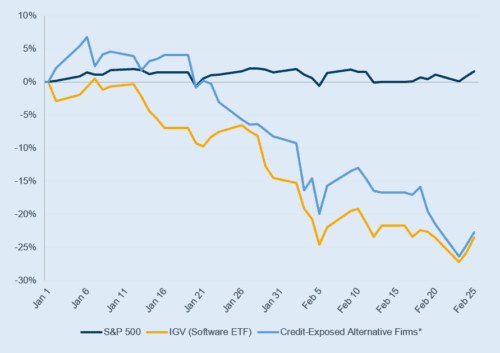

In recent weeks, we have witnessed turbulence in markets stemming from fears that AI might categorically disrupt software businesses across the board. This fear has led to public market software-related securities selling off materially in 2026. The concern is so great that private credit firms that lend to software companies have also sold off dramatically.

Exhibit 1: YTD Performance of Software Equities1

1 Source: Bloomberg. *Selected for illustrative purposes only, “Credit Exposed Alternative Firms” include Ares, Apollo, KKR, Blackstone, and Blue Owl. Use of information from sources referenced herein does not represent any sponsorship, affiliation, or other relationship between HighVista and any other company or entity and does not constitute an endorsement.

What is all this brouhaha about? Is it justified? Given the velocity of news flow related to cyclical macro conditions, geopolitical developments, and steady AI advancement, it can understandably be challenging for observers to keep up with the current themes captivating the market. Our recent conversations suggest that many investors find it hard to distill current events and why the market is specifically concerned about the impact of AI on software. To help address this question, this paper aims to provide a simple framework to explain the market’s concern about the threat of AI to software companies, and what it might mean specifically for credit investors.

Before we dive in, we should be clear upfront that this paper simply explains the market’s concern—we are not opining on whether the current selloff is overdone/underdone or the prospects of any individual company. Arriving at any conclusion about that would result in a longer discussion—one that we would be happy to have with anyone interested.

Software 101

To start off, keep in mind that software businesses exhibit characteristics that are unique relative to traditional, run-of-the-mill businesses. Specifically, the software business model is predicated on three core assumptions:

- Front-Loaded Costs: The software R&D/Capex lifecycle is front-loaded; significant upfront spending is required to build the core product. However, once the product is shipped, R&D intensity diminishes greatly (especially relative to revenue) as the software company develops and transitions to upkeep/upgrade mode.

- Gross Margins: Similarly, gross margins are very high (90%+) because the product is entirely digital and incremental distribution costs are minimal—there are almost no traditional COGS in software. These high gross margins, coupled with highly fixed, often non-recurring costs, create a financial profile with a lot of native operating leverage.

- Recurring Revenue: Customers are very sticky. Subscription software revenue is highly recurring, as onboarding a software solution typically requires up-front costs such as building customized linkages within the organization’s technology stack and training staff to use it, such that switching providers is a burden that many seek to avoid. This aspect of software works together with the prior points to justify not only high initial development expense but also high ongoing selling costs, which can be expended upfront to hopefully create a trail of high-margin, highly recurring revenue for years to come.

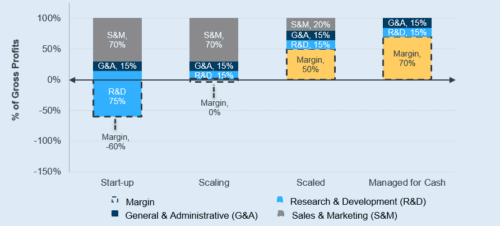

These three factors result in a business structure that is highly scalable and predictably profitable upon achieving scale. Moreover, it also allows for tactical financial control via a “profitability lever” that can be seemingly managed at will. Since a substantial amount of spending in any given year is used in service of growing revenue and profits in future years, these costs can be cut back if growth expectations fall or current cash flow is needed. For these reasons, software companies are valuable even if they are not profitable and are often valued on a multiple of annual recurring revenue (ARR), despite EBITDA being non-existent or even negative.

Exhibit 2: Illustrative Margins Across Lifecycle Stages2

2 Source: HighVista. Provided for informational purposes only, this illustration does not reflect any specific company.

In this way, valuing software companies on ARR can be thought of as a shorthand for valuing on a traditional metric such as EBITDA, as investors will apply an assumed “steady state margin” that is not burdened by S&M or R&D costs. For example, if you assume a 50% EBITDA margin at scale (or when managed for profitability) and a software company is worth 5x ARR, it is analogous to saying that it is worth a 10x “effective” EBITDA. This shorthand has become common in the software industry for investors of all types. In credit markets specifically, where lenders would typically lend against cash flow, the industry has developed comfort lending against ARR.

These three inherent features make software businesses a very special class of company and partly explain why software has created a tremendous amount of economic value, driving multiple expansion and widespread adoption as mainstay allocations for equity and credit investors across both public and private markets.

AI as a Paradigm Shift

So, what’s the problem? Markets have recently recognized AI as being a fundamental threat to the software business model because it attacks each of the three core tenets that make software businesses work:

- Front-Loaded Costs: AI has the potential to reset the R&D/Capex lifecycle for software companies. Regardless of how mature a software platform is, customers expect that their software solutions will be AI-enabled in the future. Those that fail to implement AI capability sufficiently may become irrelevant and face declining prospects. This has the practical effect of forcing a reset in the R&D cycle for most software businesses that now require large expenditures of capital to remain relevant—and, in some cases, companies may need to completely redesign how their core product works to remain competitive.

- Gross Margins: AI is not free, as it requires that compute/power be paid for on an ongoing basis, and, in fact, the more that it is used, the higher these costs will be. Therefore, the more a software solution is AI-enabled, the more it may have an increasingly embedded “cost of goods sold”. This suppresses the gross margin of the software business and would tend to structurally lower its margin potential vis-à-vis a pre-AI world.

- Recurring Revenue: AI has the potential to dramatically erode the strong customer retention that software businesses rely on in the current paradigm. While customers historically have been hesitant to switch software providers, AI has the potential to chip away at this stickiness on numerous fronts:

- AI, which has already made significant improvements, is currently the worst it will ever be and will only get better. The simple competitive threat of superior products emerging, either from new companies or existing companies expanding their capabilities, has increased for any given software company.

- AI itself may alleviate the switching costs of software, reducing customer friction.

- AI may fundamentally change the nature of how customers interact with software, rendering many existing products irrelevant. For example, agentic AI may displace the user-software paradigm in some cases, rendering legacy software unsaleable at any price.

If any one of these three pillars no longer holds true, the value proposition and valuation frameworks applied to software should be called into question. Yet AI is attacking all three pillars at the same time! This creates a great deal of future uncertainty, which is not the friend of high-multiple, long-duration assets with little upfront cash flow. To be sure, some software companies will transition to become AI winners and be worth well north of where they are valued today. But many will be losers, and this is what the market is worried about.

Is the market right or wrong? We can’t say with a broad brush. For every aspect of AI that threatens software, there might be a silver lining that enhances it. For example, AI has the potential to lower the cost of R&D incrementally. Compute costs might go up, but if value-add is high, customers are more likely to be happy to pay more. If companies have proprietary data, layering in AI could dramatically increase switching costs instead of the opposite. So far, we haven’t seen much degradation in the operating metrics of the companies we track, but the proverbial game has only just begun. What we do know is that the factors the market is concerned about, which we have outlined above, make total sense to us, and it will be up to investors to sort out the specifics for any given company.

Given all that, it is perhaps an exciting time to be in software. The advent of AI offers an unprecedented opportunity to innovate and drive value. To do so, companies need strong management teams and a relentless focus on product innovation. In addition, they need financial resources and balance sheet flexibility to embark on the investment cycle. Fortunately, many software companies, especially those in public markets, have significant levels of cash and access to capital, and can use these resources to seize the moment.

Implications for Credit Investors

Unfortunately, credit investors with software exposure face two potential problems. First, the increased volatility caused by this paradigm shift could hurt lenders as a class. This is because lenders have capped returns if things go right but are exposed to total loss of capital if things go catastrophically wrong. This is a problem. Imagine that AI causes half of software companies to be worth double and the other half to be wiped out completely. In that scenario, creditors as a class will lose, whereas equity investors might be fine. In other words, increasing volatility is not a friend to lenders.

Second, we think that software companies need financial flexibility to capture the moment—and that is not something that many software borrowers in the private credit markets have much of. Instead of having piles of free cash, these companies, definitionally, have significant debt that must be serviced, and lenders are becoming more restrictive by the day. For these borrowers, the existence of high debt loads will tend to divert valuable resources that are needed to invest in R&D to instead pay debt service. We also would not be surprised if the highly indebted companies also have hidden issues with “technical debt” vs. less-levered counterparts. This poses a problem for equity holders—but debt holders may not be spared either. Remember that many of these companies lack sufficient cash flow (recall the shorthand of lending against ARR vs. actual cash EBITDA) to amortize existing debt burdens. Therefore, lenders will need to be paid back through potential sales or refinancings of their borrowers at a time when fundamental business uncertainty is peaking and multiples are compressing. The catch-22 for lenders is that while they can force their software borrowers to cut costs and deliver near-term cash flow, it may not be enough to fully amortize debt and will paradoxically come at the expense of innovation that may sap the borrower’s terminal value.

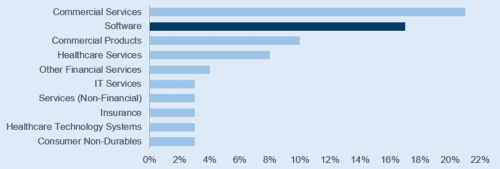

These structural concerns are compounded by late-cycle macro considerations affecting the broader credit markets. With that in mind, it does make sense that markets have discounted traded software credit portfolios and their proxies, such as the credit-exposed alternative firms referenced above in Exhibit 1, or the software-exposed BDCs as illustrated in Exhibit 3 below. Again, we are not commenting on whether the quantum of any repricing is correct, but we think the direction probably is.

Exhibit 3: Count of BDC Holdings by Sector (%)3

3 Source: PitchBook │LCD ● Data through Sept. 30, 2025

HighVista Positioning

The dynamics discussed above highlight a central reality for credit investors. Today’s period of technological disruption introduces new risks that investors must consider and should exercise caution when proceeding. As outcomes become more dispersed and visibility less certain, the margin for error narrows. In those environments, underwriting standards matter more, not less. At the same time, opportunity is likely to present itself to those who can manage their portfolio and take advantage of dislocations stemming from the age of AI.

Against this backdrop, HighVista’s Private Credit program has remained intentionally selective, and we are fortunate to report that our private credit portfolio has very minimal direct exposure to software and software-related investments. This positioning reflects our long‑standing emphasis on discipline and selectivity rather than a reactive response to recent developments.

HighVista’s approach to specialty private credit is grounded in disciplined underwriting, strong structural protection, and a focus on downside risk across market cycles. In the context of software and AI, we believe this philosophy supports a cautious and selective posture, while recognizing that go-forward returns for creditors may improve if lenders pull back from the sector. We also believe rapid technological change can amplify dispersion in borrower outcomes, and that uncertainty warrants a higher underwriting bar for lenders. We prioritize opportunities where returns are driven by durable cash generation, conservative leverage, and creditor‑friendly structures.

In software, as across other markets and environments, our objective remains consistent: we aim to protect capital, generate strong contractual returns, and build robust all-weather portfolios for our partners.

Important Disclosure

This presentation is provided for informational purposes only, is general in nature, and is meant only to provide a broad overview for discussion purposes. The information expressed herein reflects the judgments and opinions of the authors at the time of writing, does not purport to be complete, has been excerpted from HighVista investor communications, and no obligation to update or otherwise revise such information is being assumed. Historical data, statements, and other information contained herein is believed to be reliable but no representation or warranty is made as to its accuracy, completeness or suitability for any specific purpose. Some information used in the presentation has been obtained from third parties through various published and unpublished sources. HighVista does not warrant the accuracy, adequacy, or completeness of the information and materials contained in this document and expressly disclaims liability for any expressed or implied representations, errors, or omissions in such information, materials or any related written or oral communications transmitted to the recipient. Use of information from sources referenced herein does not represent any sponsorship, affiliation, or other relationship between HighVista and any other company or entity and does not constitute an endorsement. This information does not constitute, and should not be construed as, an offer of advisory services, securities or other financial instruments, a solicitation of an offer to buy any security or other financial instrument, or a recommendation to buy, hold or sell a security or other financial instruments in any jurisdiction. Any reproduction or distribution of this presentation, in whole or in part, or the disclosure of its contents, without the prior written consent of HighVista Strategies LLC is prohibited.

References to specific securities, issuers, indexes, and strategies are for illustrative purposes only, does not represent any sponsorship, affiliation, or other relationship between HighVista and any other company or entity, does not constitute an endorsement, and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Nothing contained herein constitutes investment, consulting, legal, tax, accounting, or other advice, nor is it intended to be relied on in making an investment or other decision. Information provided herein is based upon HighVista data and analysis and is believed to be accurate as of the time of writing, but no representation or warranty is made herein. Statistical and mathematical measures of performance and risk measures based on past performance, market assumptions or any other input should not be relied upon as indicators of future results. While HighVista Strategies LLC believes the assumptions and possible adjustments it may make in making the underlying calculations are reasonable, other assumptions, methodologies and adjustments could have been made that are reasonable and would result in materially different results, including materially lower results. The strategies described in this presentation may exhibit the potential for attractive returns, however they also involve a significant degree of risk, including the risk of total loss of investment. A broad range of risk factors, individually or collectively, could cause a strategy to fail to meet its investment objectives No investment process, strategy, or risk management technique can guarantee returns or eliminate risk in any market environment.

THIS PRESENTATION CONTAINS FORWARD-LOOKING STATEMENTS WITHIN THE MEANING OF THE U.S. FEDERAL SECURITIES LAWS. FORWARD-LOOKING STATEMENTS ARE THOSE THAT PREDICT OR DESCRIBE FUTURE EVENTS OR TRENDS AND THAT DO NOT RELATE SOLELY TO HISTORICAL MATTERS. FOR EXAMPLE, FORWARD-LOOKING STATEMENTS MAY PREDICT FUTURE ECONOMIC PERFORMANCE, DESCRIBE PLANS AND OBJECTIVES OF MANAGEMENT FOR FUTURE OPERATIONS, PERFORMANCE AND RISK AND MAKE PROJECTIONS OF REVENUE, INVESTMENT RETURNS, RISK CALCULATIONS OR OTHER FINANCIAL ITEMS. FORWARD-LOOKING STATEMENTS CAN GENERALLY BE IDENTIFIED AS STATEMENTS CONTAINING THE WORDS “WILL,” “BELIEVE,” “EXPECT,” “ANTICIPATE,” “INTEND,” “CONTEMPLATE,” “ESTIMATE,” “ASSUME,” “TARGET” OR OTHER SIMILAR EXPRESSIONS. SUCH FORWARD-LOOKING STATEMENTS ARE INHERENTLY UNCERTAIN, BECAUSE THE MATTERS THEY DESCRIBE ARE SUBJECT TO KNOWN (AND UNKNOWN) RISKS, UNCERTAINTIES AND OTHER UNPREDICTABLE FACTORS, MANY OF WHICH ARE BEYOND CONTROL. NO REPRESENTATIONS OR WARRANTIES ARE MADE AS TO THE ACCURACY OF SUCH FORWARD-LOOKING STATEMENTS.